The Real Cost of Waiting for the Market to Shift Before Buying Your Home

The Real Cost of Waiting for the Market to Shift Before Buying Your Home

Something we hear frequently right now is that people are waiting for the market to shift before deciding to make a move. There are a lot of life events that come into play in life that affect when it's the right time to buy a house, and waiting is sometimes the best strategy. However, I think there are a lot of people waiting for a crash or a shift in the market or for it to be a better time to be a buyer. I think that's the wrong strategy.

Today I'm talking to the people trying to ride this thing out and the people that want to strike while the iron's hot. If that's you, stick around; we'll go over numbers and talk about why now may be the best time for someone like you to get into the market.

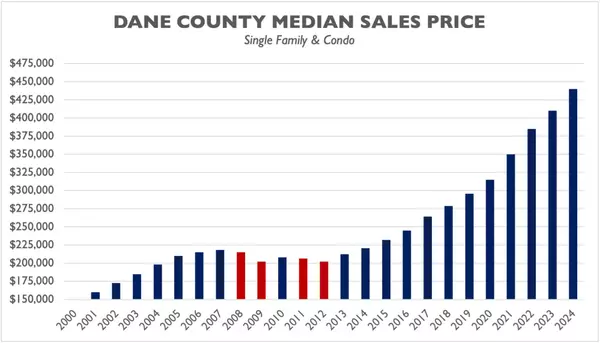

We are currently on the verge of entering the first quarter of 2022. If we take a look at some basic numbers over the last four years, you'll see that in each quarter we've seen an increase in the median sales price of housing. In fact, over the last three years, we've seen prices at seven to 10% higher for the median in sales price by the end of June when compared to the end of the previous year. An increase of seven to 10% in six months? That's huge.

On top of general appreciation, there's always conversation about interest rates. There's often the dooms day thoughts of "rates are going to go up" and "this is the year that rates change". I can tell you, though I've heard this story consistenly over the last number of years without much actual change, experts seem fairly confident that it's actually going to happen this year.

Let's look at a chart provided by Fairway Mortgage Company; this is the predicted mortgage forecast from a number of experts. You'll see Fannie Mae and the National Association of Realtors have us at 3.1 or 3.5, whereas the Mortgage Brokers Association and Freddie Mac have us up at 3.7. So, no matter how you cut it, short of the Fannie Mae prediction, everybody else predicts an increase in rates. If that happens, there will be a major impact on what you're able to do within the housing market.

Let's take a look at a sample scenario. Imagine you are a person who is pre-approved to purchase a house for $400,000 with 10% down. In other words, the maximum principle and interest payment that you're allowed to have is going to be about $1,567 a month. This assumption also includes you're at 3.25% interest rate.

Let's take a look at these sample numbers and see what happens when we bump that rate up to 3.75% to help us understand what we may be seeing this summer.

By this summer, that house is going to appreciate. So, that same house is now no longer valued at 400,000, it's $424,000 or $428,000 or $440,000, depending on where that appreciation rate goes. So, let's go at the low end, let's say 6% appreciation, which would be about the lowest we've seen over the past few years. Now, not only is the price of this house up to $424,000, but the interest rate has also gone up. It's up to 3.75%, which means your monthly payment is now about $1,767 per month. In other words, your payment has gone up about $200 a month for the same exact house, just because of appreciation and interest rates.

The reality is you may not qualify for that monthly payment amount. If you're still approved at $1,567 we now have a different situation. Because of the rate increase, you can now afford less house. Which means, if you're trying to keep that monthly payment around $1,567 a month, and rates are up to 3.75%, you can now purchase a $375,000 house. Wait, there's more. Don't forget that by this summer that $375,000 house has also appreciated. So, what you're looking at in reality is roughly a $350,000 house today if waiting until summer to purchase. In other words, you've lost about $50,000 in purchase power by waiting until this summer to buy.

What if this isn't the year that rates go up? Let's acknowledge that thought and take a look.

It's probably unlikely that this will be the year that house prices don't increase as we've seen seven to 10% median sales price appreciation over the last few years, and we still have a significant shortage of available houses. As a result, we expect to see prices rise once again this year.

Let's look at that same 3.25% interest rate, 10% down, $400,000 purchase price. The interest rate remains the same but the house has appreciated. So, the house you can actually afford by June is $360,370; you've cost yourself $30,000 to $40,000 in purchase price, just because of the appreciation.

So, what does this all mean? Well, if you're waiting for life events to occur, then by all means, wait. If you're waiting for that baby to come, that wedding to happen, that new job to take hold, or some other life situation is causing you to wait, by all means, live your life, do that thing. But, if you know you're in the market and you know you're going to purchase, and maybe you're just waiting it out, or trying to decide if this summer would be a better option, now is the time.

People buy and sell homes in all markets, so don't let this forecast scare you. If you're waiting for the crash, stop - it's not going to happen this year. By the time the market does balance out and become a favorable market for buyers, prices and interest rates will have gone up, and by then, you're going to end up spending more money for less house than if you do it today.

If you want to talk numbers or look at your unique situation, let us know. We're happy to run some numbers and look at some possibilities and scenarios that could affect your decision making. We want to make sure that you make the right decision for you, whatever that may be. Let's talk soon.

Categories

Recent Posts

GET MORE INFORMATION